Monarch Cement is a Kansas based producer of Portland cement with an operating history spanning over 114 years and an uninterrupted dividend history since 1922. Interestingly, the business has been led by the Wulf family for more than a century, with third-generation CEO Walter H. Wulf Jr. currently presiding over operations.

Monarch is headquartered in Humboldt, Kansas and its plant is capable of producing in excess of one million tons of cement per year. In addition, the plant is situated on 5,000 acres of land and Monarch believes there is sufficient raw material reserves to maintain operations at the plant for more than 50 years.

Furthermore, the company also has several subsidiaries engaged in the business of ready-mixed concrete, concrete products and sundry building materials, which ensure there is always demand for the companies cement.

Monarch sells its cement to a limited market area which includes: Kansas, Iowa, southeast Nebraska, western Missouri, northwest Arkansas and northern Oklahoma. Importantly, due to the low value-to-weight ratio of cement, it’s uneconomical to transport it beyond certain distances. Thus, Monarch is limited to this region. However, this is not a weakness of the business, it’s actually a massive strength because it creates a captive market.

Essentially, Monarch is located smack-bang in the middle of the United States, which makes it completely insulated from the seaborne trade of cement from foreign competition. So, whilst it can be economical to import cement to a coastal region, such as California, the cost per-mile of shipping in-land from California to Kansas (1,400 miles) is fruitless. As a result, foreign competition will never reach their markets nor influence local prices.

Moreover, in terms of durability, you’ll be hard-pressed to find a company more durable than Monarch Cement. As mentioned, they sell a product with a low value-to-weight ratio, which makes it a very attractive commodity from a competitive standpoint. However, it’s also an attractive commodity because of its popularity. Importantly, cement is the binding ingredient that gives concrete its well-known strength; which consequently makes cement the most widely used construction material in the world. In fact, twice as much concrete is used in construction than all other building materials combined!

Furthermore, if you’ve ever studied the Romans you’ll know they were big proponents of using concrete to build their legendary buildings, such as the Pantheon (which still stands tall 2000 years later!). Of course, ancient Roman cement and modern Portland cement are different, but fundamentally they are the same. So, whilst it might not get the recognition it deserves, concrete is arguably the foundation of modern civilisation – it’s built our roads, buildings and bridges, and I suspect will continue to do so for a long time to come.

Now, if Monarch Cement is so ideally located, and if the cement industry is so good, then why isn’t someone trying to build a competing plant? Well, the business is characterised by very high fixed-costs which means it’s essential to maintain a certain level of sales to remain profitable (hence, supply has to remain low). For example, if you did build a competing plant you’d instantly double local supply. However, you wouldn’t double demand. Thus, the eventual outcome is both plants would be operating at around 50% utilisation rates and neither would be generating sufficient returns. So, you could compete with Monarch Cement, but it’d be self-destruction. Also, not to mention, cement plants make for terrible neighbours, so getting building approval is a difficult proposition (it’s no surprise Monarch is over 100 years old!).

Nonetheless, the business is heavily dependent on the construction industry and changing levels of activity can drastically effect the business. As a result, it is an inherently cyclical business, due to the construction industries tie to the wider economy. For example, during the financial crisis, cement production declined by 35% peak-to-trough, with most plants operating at below 60% utilisation rates. However, during this period, Monarch Cement was largely insulated from the wider recession in construction due to its rural location. In fact, sales increased in 2008 by 5% whilst gross profit only declined 3% (the business fared slightly worse in the latter years but remained profitable). So, Monarch never really felt the effects of the housing bubble, but that doesn’t insure it protection from future recessions. However, it does suggest its advantageous location insulates it far better than most of its peers.

Importantly, the basis for competition is price because there is no difference in the quality of cement between producers. Thus, producers need to be as efficient as possible to reduce production costs and keep prices low. Of course, the easiest way to achieve this is by scale. Hence, the industry is slowly consolidating overtime and the market share of the largest players is growing. Currently, the major US producers have around 40% market share (source: IBIS World).

Monarch is a minor player, but it’s so well situated that it’s been able to maintain a dominant position within its local market and not worry about foreign competition. US cement producers want to ensure capacity remains low to maintain high utilisation rates. Consequently, major US cement producers aren’t going to want to add local capacity in Monarch’s markets; meaning the status quo will remain. In fact, the only way a cement producer can enter an existing market is by acquiring the existing producer(s), which is why the industry is consolidating overtime.

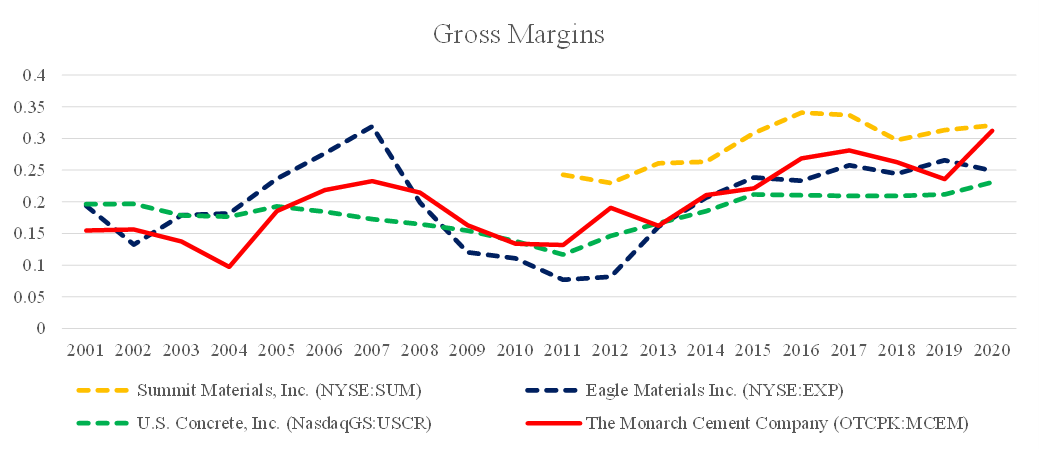

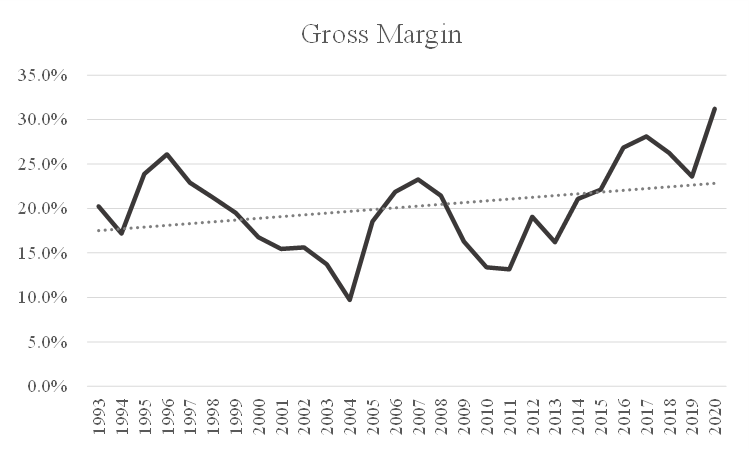

As shown, the business has been growing sales historically at around 2-4% per annum which has been driven by both price and volume increases. So evidently, the high barriers to entry have allowed the company to maintain strong local market share and capture the underlying growth in demand. Also, the company’s gross margins have been relatively stable, suggesting they have a strong cost position versus competitors.

Monarch Cement is a capital intensive business that requires significant investment in property, plant and equipment. Also, it needs a trained workforce to maintain and operate this equipment. Hence, regardless of production levels, costs will not change significantly in response to lowered sales. In fact, operating at lower production levels can actually create inefficacies that can increase costs. Consequently, during periods of declining sales, the company experiences significantly higher per unit production costs. Nonetheless, in 2010 & 2011 (which was one of the worst periods of reduced demand in cements history) the business managed to maintain ~13% gross margins, which was only a 1000bps decline from its peak in 2007 (23%). Thus, even in bad years, the business has maintained profitability and managed per unit production costs effectively.

Of course, the flip side of the largely fixed production costs, is that once Monarch Cement surpasses a certain level of production volume (~700K tons), the profits the business can generate increase significantly due to operating leverage.

Moreover, in terms of returns on capital, the business has generated an average return on equity over the past two decades of 10%; with absolutely minimal use of debt. For example, Eagle Materials Inc. generated a 16.6% return over this period but its average debt/equity ratio was 57.7% versus 14% for Monarch Cement. Hence, if Monarch was less conservative and increased leverage, it could easily be generating returns as high as its peers. Nonetheless, a 10% return on equity is a very reasonable return, and over a long enough holding period it would likely be a fairly good predictor of the stocks return.

Furthermore, as shown, the returns of the business largely track the gross margins, which suggests that the predominant driver of returns is the per unit production costs of the business. Thus, we can observe that as the business has improved cost efficiencies overtime (by achieving economies of scale), the returns on equity have improved correspondingly. Moreover, it is apparent during periods of lesser demand, when per unit production costs are high, returns suffer. Consequently, in the long run, the predominant determinant of returns will be the businesses ability to keep per unit production costs low. Therefore, considering the high barriers to entry and the continuing industry concentration, Monarch Cement will be facing significantly less competition in the future and will have a stronger competitive position going forward. As a result, it is likely that returns should fare well going forward.

In 2020, Monarch Cement generated $33.9 million in net income (which was higher when ignoring unrealised losses on their equity portfolio). Furthermore, the company retained approximately 77% of earnings and invested $23.5 million into property, plant and equipment; with the majority being maintenance capital expenditures. Due to the nature of the business, Monarch retains the vast majority of earnings and reinvests it into capital expenditures to keep the business operating efficiently. For example, Monarch recently improved their kilns so they could burn fuel more efficiently and reduce costs. Thus, going forward the company will continue to retain the majority of earnings and reinvest it into capital expenditures.

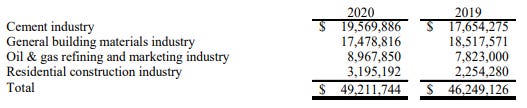

The remaining earnings are paid out as dividends and the excess cash is usually re-invested into the company’s portfolio of equities. Interestingly, the portfolio largely consists of its peers such as Eagle Materials, Summit Materials and other similar companies. Walter H. Wulf Jr. doesn’t have any particular prices he prefers to buy at, he has simply been dollar cost averaging when the company has excess cash; today the value of the portfolio is $49 million (not bad!).

Again, Monarch Cement has been in operation for 114 years, and the same family has been running it for almost the entirety of that time. So, they’ve seen the market cycles and they know how to prepare for them. It’s an extremely experienced management team that knows the business like the back of their hand, and Walter H. Wulf Jr. has inherited the experience of both his grandfather and father. Consequently, you can be confident the company is going to continue running the business like it has for decades.

Valuation

As mentioned, the only way a cement producer can really enter an existing market is by acquiring the existing plants. As a result, the price a private buyer will pay to acquire an existing plant is significantly higher than both the replacement cost and the current public market price. Thus, to know how much Monarch Cement might be worth it’s important to figure out how much a private buyer would pay for the company. Fortunately, there are several existing acquisitions in recent history that gives us a pretty reasonable predictor of how much Monarch Cement is actually worth. In 2017, CRH plc (one of the world’s largest building material companies) acquired the national cement producer Ash Grove for $3.5 billion, which valued the business at 10x EBITDA. Furthermore, in 2019, Eagle Materials acquired Kosmos’ Louisville, Kentucky cement plant for $665 million. Interestingly, Kosmos’ plant had a capacity of 1.7 million tonnes per year and Eagle Materials also acquired seven distribution terminals plus substantial raw material reserves; the total price paid amounted to a 12x EBITDA multiple.

Furthermore, if we look at the historical price that Summit Materials has paid to acquire companies it’s been approximately 8x EBITDA. So, we can reasonable suggest that Monarch Cement’s private buyer value is somewhere within the range of 8-12x EBITDA.

Currently, Monarch trades at a share price of $109, which values the company at 6x EV/EBITDA. Therefore, if we assume the true value of Monarch Cement is closer to 10x EBITDA, it would imply a ~60% upside from its current valuation.

Also, whilst it’s often not wise to bank on a family-owned business selling, it is noteworthy that Walter H. Wulf Jr is 75 and he’s the last Wulf family member on the board; suggesting there is no successor. So, perhaps he’s seen the recent acquisitions of Ash Grove and Kosmos, and maybe for the right price he’d be inclined to sell. I’m not entirely certain, but it’s clear if it was to happen, the price being paid would be significantly higher than the price being offered by the market.

Monarch Cement also appears cheap on a relative basis. In fact, its peer’s trade for an average of 13x EV/EBITDA, versus Monarch Cement at an EV/EBITDA of 6x. However, Monarch doesn’t file with the SEC and the stock is fairly illiquid, so it should trade at some discount. Nonetheless, the company certainly looks undervalued based on the price the market is offering.

Overall, I think Monarch Cement is undoubtedly undervalued. However, for that value to be realised the company would have to sell. I don’t think Monarch Cement is going anywhere in a hurry.

In conclusion, Monarch Cement is a company I’d like to own and hopefully I’ll eventually get the chance, but for now I’ll sit on my hands and continue learning about the company.